Picture a regional employer running entities in Dubai and Riyadh simultaneously. Mid-year, its Dubai office receives an MOHRE compliance flag for missing Emiratisation headcount. That same quarter, the Riyadh entity was downgraded to Low Green under Nitaqat, blocking new visa applications at a critical hiring moment. Two countries, two enforcement bodies, two separate penalty structures, and no single fix that works for both. This situation, increasingly common for GCC-wide businesses, is exactly why understanding GCC workforce nationalisation as a comparative discipline — not just country by country — is essential for HR and operations teams in 2026.

Every Gulf Cooperation Council state runs its own workforce nationalisation programme, each with a distinct legal framework, enforcement mechanism, and target sector mix. Whether you are building a compliant talent strategy for one market or all five, understanding what each programme actually demands of private sector employers is the starting point. Our HR services for GCC businesses can also help you structure this across jurisdictions.

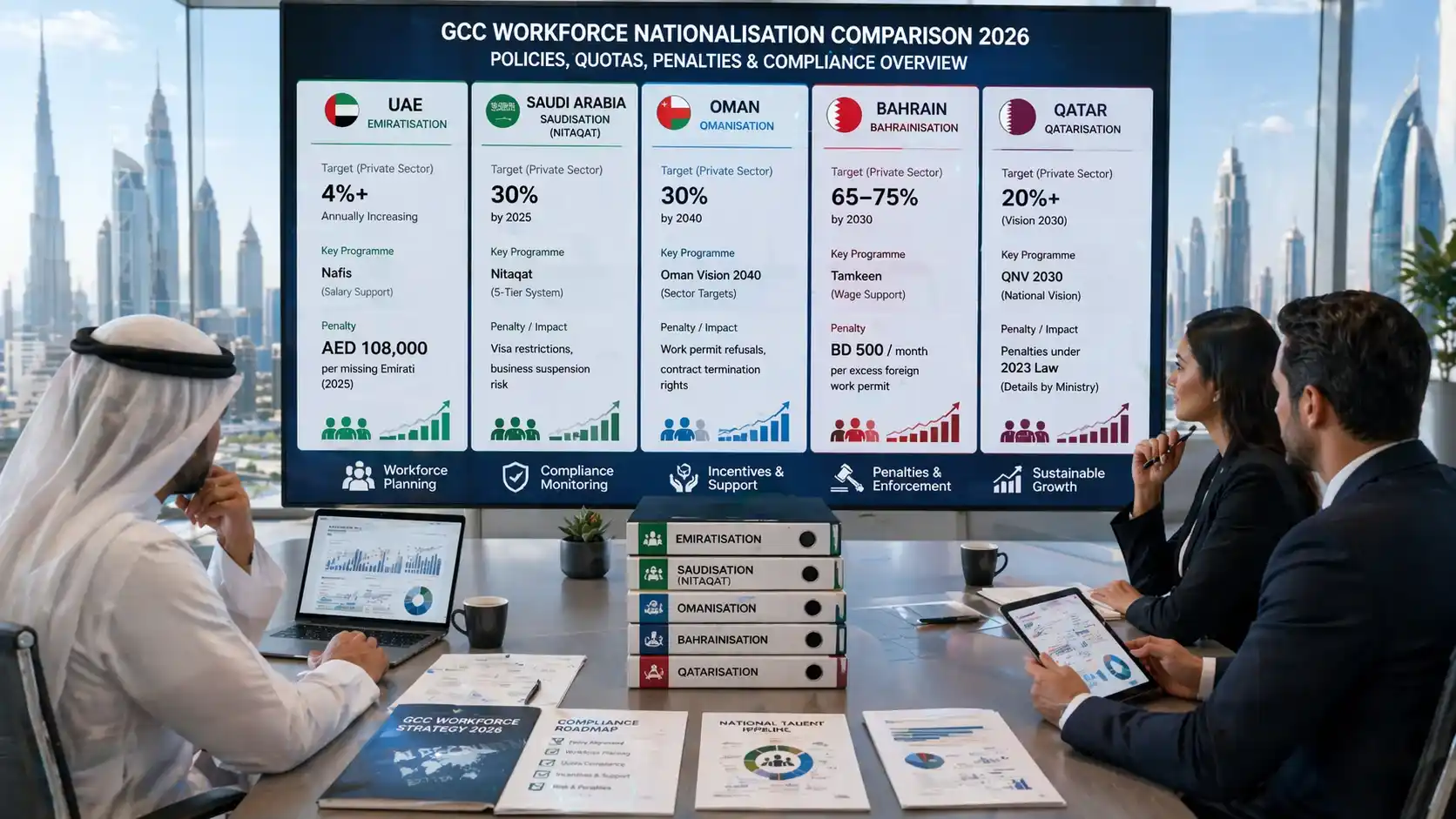

GCC Workforce Nationalisation: The Five Programmes at a Glance

|

|

UAE |

Saudi Arabia |

Oman |

Bahrain |

Qatar |

|

Programme name |

Emiratisation |

Saudisation (Nitaqat) |

Omanisation |

Bahrainisation |

Qatarisation |

|

Vision framework |

UAE Centennial 2071 |

Vision 2030 |

Oman Vision 2040 |

Economic Vision 2030 |

Qatar National Vision 2030 |

|

Enforcement body |

MOHRE |

MHRSD |

MCII / Ministry of Labour |

LMRA / Tamkeen |

Ministry of Labour |

|

Current localisation rate (approx.) |

~4% private sector Emiratis |

~23% (Q1 2022 baseline, targeting 30% by 2025) |

~19% (targeting 30% by 2040) |

~55% (targeting 65–75% by 2030) |

~19% (targeting 20%+) |

|

Primary compliance tool |

Quota per company size & sector; Nafis subsidy |

Nitaqat colour-zone classification |

Sector-specific ratio targets |

Quota + BD 500 monthly levy |

Quota law enacted in December 2023 |

|

Key private sector penalty |

AED 108,000 per missing Emirati (2025) |

Visa restrictions; business suspension risk |

Work permit refusals; contract termination rights |

BD 500/month per excess foreign worker permit |

Penalties under the new 2023 law (structure TBC by Ministry) |

UAE: Emiratisation — The Most Rapidly Escalating Programme in the GCC

Emiratisation is the UAE’s mandatory workforce nationalisation policy, requiring private sector companies to hire and retain UAE nationals in meaningful employment. Administered by the UAE Ministry of Human Resources and Emiratisation (MOHRE), it is currently the most actively enforced and fastest-escalating nationalisation programme in the Gulf.

For companies with 50 or more employees operating in any of the 14 targeted economic sectors — including finance, real estate, professional services, healthcare, and construction — the annual Emiratisation target has been climbing by 2% of the total workforce each year since 2022. For companies in the 20–49 employee band operating in those same sectors, the requirement is simpler but no less real: hire one UAE national by the end of 2024, and another by the end of 2025.

Penalties are substantial and escalating. The penalty for each missing Emirati national stands at AED 96,000 for the 2024 target period, rising to AED 108,000 for 2025, and increasing annually thereafter. Missing a target by five nationals means over AED 540,000 in fines. Companies involved in ‘fake Emiratisation’ — enrolling UAE nationals on paper without genuine employment — face criminal prosecution under Cabinet Decision No. 43 of 2025, and MOHRE detected 405 such cases in the first half of 2025 alone.

The Nafis incentive programme provides a meaningful counterweight. Employers who genuinely hire Emirati nationals can access government-funded salary top-ups that partially offset the cost premium of employing nationals versus expatriates. The banking sector carries a separate 45% Emiratisation target under the Central Bank’s ‘Ethraa’ programme. For employers who have not yet formalised their Emiratisation strategy, our detailed Emiratisation 2026 compliance guide covers quotas, penalties, and Nafis in full.

Saudi Arabia: Saudisation and the Nitaqat System — The Most Structurally Complex Programme

Saudisation — formally the Saudi Nationalisation Scheme — is enforced through the Nitaqat system, administered by the Saudi Ministry of Human Resources and Social Development (MHRSD). It is the most structurally sophisticated nationalisation framework in the GCC, classifying every private sector employer into one of five colour-coded compliance zones: Platinum, High Green, Medium Green, Low Green, and Red.

Your zone determines what you can and cannot do. Platinum companies enjoy the widest operational freedoms, including fast-track visa processing and priority hiring rights. Red-zone companies lose the ability to sponsor new work visas, renew existing permits, and bid on government contracts — and face the risk of business suspension in severe cases.

Sector-specific Saudisation rates are expanding aggressively under Vision 2030. From July 2025, engineering firms with five or more engineers must achieve a 30% Saudisation rate. Dentistry clinics with three or more dental professionals face 45% from July 2025, rising to 55% by January 2026. Accounting firms with five or more accountants enter a five-phase programme beginning at 40% from October 2025, climbing to 70% over five years. The Ministry also raised the marketing and sales Saudisation rate to 60% across companies with three or more employees in those roles. The MHRSD now covers Saudisation obligations across 269 professions.

A critical 2024 compliance update: foreign investors who own private establishments in Saudi Arabia are now counted as Saudi nationals in Nitaqat calculations — a meaningful change for multinational company structures. Employers must also now comply at the profession level, not just overall headcount: a company can meet its company-wide ratio but still fall into non-compliance within a specific function, such as engineering or accounting. For a detailed side-by-side view of what this means versus UAE employer obligations, our Recruiting in Saudi Arabia vs UAE comparison is the relevant companion read.

Oman: Omanisation — Expanding Obligations, Sector-Led Targets

Omanisation, overseen by the Oman Ministry of Commerce, Industry and Investment Promotion (MCII), is grounded in Oman Vision 2040’s objective of raising the national workforce participation rate from approximately 19% to 30% by 2040. The programme operates through sector-specific targets rather than a single cross-economy quota, which makes compliance obligations vary significantly depending on industry.

Sector targets include 60% for banking and finance, 35% for manufacturing, 30% for hotels and restaurants, 20% for wholesale and retail, and 15% for contracting. Banking and airline roles carry some of the most prescriptive requirements, with Omani nationals historically required to fill HR manager, secretarial, security officer, and public relations roles.

The 2024 expansion is significant for private sector employers. Ministerial Decree No. 501/2024, issued in late 2024, added over 30 professions restricted exclusively to Omani citizens — covering engineering roles, hospitality management positions, and IT functions. These restrictions are being implemented in phases between 2025 and 2027, giving employers a defined window to restructure workforce composition. From April 2024, foreign firms with more than 25 employees are also required to hire at least one Omani citizen within their first year of operations in the Sultanate. A specific provision within the 2023 labour law also permits employers subject to Omanisation to end contracts with expatriate employees in order to fulfil Omanisation obligations.

Financial incentives, potentially including direct government salary contribution, are being introduced to make Omani national hiring more commercially viable for private sector employers operating in cost-sensitive segments. Free zone companies operate under reduced Omanisation requirements, though the applicable obligations should be confirmed by the jurisdiction.

Bahrain: Bahrainisation — The Highest Localisation Rate and a Market-Led Model

Bahrain stands out among GCC nationalisation programmes for achieving the highest overall localisation rate in the region — approximately 55% of the private sector workforce as of 2021 — and for operating what analysts describe as the most market-compatible model. Unlike quota systems elsewhere, Bahrain moved away from rigid numerical mandates in 2007 toward a levy-and-incentive structure that allows market forces to influence hiring decisions while maintaining a financial pressure on employers to prioritise nationals.

The compliance mechanism is enforced by the Labour Market Regulatory Authority (LMRA) and supported by Tamkeen — Bahrain’s Labour Fund. Companies that fail to meet their Bahrainisation thresholds pay BD 500 per foreign work permit per month and are barred from participating in government tenders. Tamkeen, which is funded partly by fees collected from foreign work permits, channels its support into direct wage subsidies — covering up to 80% of salary costs for eligible categories, including workers with disabilities in 2025 — and into training and upskilling programmes aligned with the National Labour Market Plan 2023–2026.

In 2024, Tamkeen recorded its strongest-ever results: employing and supporting the career development of 41,000 Bahrainis in the private sector, including over 15,200 new employment placements and 25,700 supported through skill development programmes. Bahrain’s target is to raise the private sector localisation rate to 65–75% by 2030, and a January 2024 Shura Council law now requires employers with 50 or more workers to provide at least three months of professional training to university graduates — at a ratio of one trainee per 50 employees — as a workforce readiness obligation.

Bahrain’s unemployment rate stood at 6.16% in 2024, and the LMRA confirms that all sectors now carry Bahrainisation quotas monitored electronically. Parliamentary investigation in early 2025 recommended setting quotas for Bahrainis in private hospitals, schools, and universities, and proposed that government-owned companies should maintain at least 90% local workforces.

Qatar: Qatarisation — A Policy Accelerating After Decades of Slow Progress

Qatarisation, aligned with Qatar National Vision 2030 (QNV 2030), has existed in policy form since 2000 but spent its first two decades concentrated almost exclusively in the oil and gas sector. Private sector Qatarisation, by most measures, remained limited: the workforce nationalisation rate stood at approximately 19% as of 2022, with 85.7% of unemployed Qataris — according to Planning and Statistics Authority data — reporting unwillingness to work in the private sector.

That landscape is changing. The Qatar Ministry of Labour oversaw the passage of a new Qatarisation law in December 2023, approved by the Cabinet and applicable to private sector entities, including commercial companies, companies partially owned by the state, and companies wholly in private ownership. The law requires private entities to employ, train, and qualify Qatari citizens actively seeking work. Where no eligible Qatari applicant is available, employers must give priority to the children of Qatari women. The Ministry is charged with publishing a full Qatarisation plan — covering training, employment, qualification, and university scholarship pathways — and reporting annually to the Council of Ministers on progress.

Qatar has invested substantially in raising educational quality and tertiary enrolment, with strong growth in nationals entering higher education since 2006. However, the mismatch between educational output and private sector demand remains a structural challenge: most Qatari graduates pursue humanities, social sciences, or business degrees, while private sector demand trends toward technical and operational roles. Qatarisation has historically produced results in oil and gas and manufacturing, but has underperformed in finance, real estate, and emerging sectors like IT and healthcare. The 2023 law is designed to address this gap systematically, though the specific quota structures and enforcement mechanisms are still being formalised by the Ministry.

What All Five Programmes Share: The Common Challenges

Despite meaningful structural differences, GCC workforce nationalisation programmes share a set of recurring challenges that employers must plan around:

• Public sector preference: In all five GCC states, nationals disproportionately prefer public sector employment, which typically offers higher wages, shorter hours, and greater job security. Private sector employers cannot simply hire to meet quotas without also addressing why nationals stay.

• Skills mismatch: Education systems across the region have historically produced graduates whose qualifications do not align with private sector demand — particularly in technical, engineering, and digital roles. All five governments are addressing this through vocational reform, though the gap remains significant in the near term.

• Retention risk: Compliance is not a one-time achievement. In the UAE, an Emirati who leaves resets the quota count immediately. In Saudi Arabia, a Saudi national’s departure drops the Nitaqat percentage in real time. Building retention into the nationalisation strategy is as critical as the initial hire.

• Fake employment risk: Ghost employment — enrolling nationals on paper without genuine roles — is a risk that all five governments are actively combating. In the UAE, it now carries criminal liability. In Bahrain, Tamkeen conducts over 15,000 inspection visits annually to beneficiary companies from 2025 onwards.

• Overlapping compliance for multi-country employers: Companies operating across GCC borders face different rules in each jurisdiction simultaneously, with no single cross-GCC compliance standard. Jurisdiction-specific HR planning is not optional for regional businesses.

Employer Implications: Planning Across GCC Nationalisation Requirements

For multi-market GCC employers, the most effective approach treats nationalisation compliance as a standing HR function rather than a periodic response to enforcement. That means:

• Maintaining a per-country compliance map updated at least semi-annually, since quotas change in Saudi Arabia and the UAE on defined schedules, and enforcement tightens incrementally

• Identifying sector-level obligations — not just company-wide ratios — especially in Saudi Arabia, where profession-specific Nitaqat targets now exist independently of overall headcount ratios

• Accessing available incentive mechanisms: Nafis in the UAE, Tamkeen wage support in Bahrain, and the emerging financial incentive structures in Oman can meaningfully reduce the cost burden of compliance

• Building national talent pipelines rather than reactive hiring: the companies achieving sustainable compliance across GCC markets are those that have invested in structured onboarding, mentoring, and career development for national employees — reducing the churn that resets compliance counts

For companies that need to map their current exposure across one or more GCC jurisdictions, a multi-country HR compliance audit is the recommended starting point.

Frequently Asked Questions

What is the difference between Emiratisation and Saudisation?

Emiratisation (UAE) and Saudisation (Saudi Arabia) are both mandatory workforce nationalisation programmes requiring private sector employers to hire a specified percentage of nationals. The key structural difference is the enforcement mechanism: Emiratisation operates through fixed per-missing-national financial penalties (AED 108,000 per missing Emirati in 2025) and a biannual review cycle. Saudisation uses the Nitaqat colour-zone classification system, where a company’s compliance band determines its ability to process visas, renew permits, and bid on contracts — operational restrictions rather than a simple fine.

Which GCC country has the highest nationalisation rate?

Bahrain has achieved the highest private sector localisation rate among the five GCC states compared in this article — approximately 55% as of 2021, targeting 65–75% by 2030. This is largely attributable to Bahrain’s market-based approach, combining a levy on foreign workers with Tamkeen’s substantial wage support and training subsidies, rather than purely a punitive quota system.

Do GCC nationalisation rules apply to free zone companies?

This varies by country and free zone. In the UAE, free zone companies are generally not subject to mainland Emiratisation requirements, though DIFC and ADGM have their own employment frameworks. In Saudi Arabia, free zone and special economic zone status does not provide a blanket exemption from Saudisation where substantive operations and staffing exist on the ground. In Oman, free zones carry reduced Omanisation requirements. Employers should confirm the applicable obligations for each jurisdiction and zone before structuring operations.

What are the penalties for non-compliance with Bahrainisation?

Companies that fail to meet Bahrainisation targets in Bahrain are charged BD 500 (approximately USD 1,325) per foreign work permit per month. They are also barred from participating in government tenders and may face blocks on their ability to post vacancies through the National Employment Platform. Repeated or egregious non-compliance can also affect LMRA classification and access to Tamkeen support programmes.

Is Qatarisation enforced in the same way as Emiratisation?

Not currently. Qatarisation is at an earlier stage of formal enforcement than Emiratisation. The December 2023 law established the legal basis for private sector Qatarisation requirements, but the Ministry of Labour is still developing the specific quota structures, sector targets, and penalty mechanisms. Employers operating in Qatar should monitor Ministry guidance closely, as the framework is expected to become more prescriptive through 2025 and 2026.

Conclusion

GCC workforce nationalisation is not a single policy — it is five distinct regulatory systems operating simultaneously, each with its own compliance logic, enforcement intensity, and employer obligations. The UAE’s Emiratisation is the most financially punitive for non-compliance. Saudi Arabia’s Saudisation is the most structurally complex. Bahrain’s Bahrainisation has the highest achieved localisation rate and the most market-compatible design. Oman’s Omanisation is expanding rapidly through the 2024 ministerial decrees. And Qatar’s Qatarisation is entering its most active enforcement phase after decades of limited private sector impact.

For employers operating across the Gulf, the gap between understanding nationalisation in principle and managing it in practice is significant. If you need to assess your current exposure, build a compliant hiring strategy, or find and hire the right talent across the GCC, ReapHR works with regional and international businesses across all five markets covered in this guide.